The Reverse Charge Mechanism (RCM) is a provision under the Goods and Services Tax (GST) framework where the responsibility for paying tax shifts from the supplier to the recipient of goods or services. Unlike the traditional tax model, where the supplier is liable to pay the tax to the government, RCM requires the recipient to pay the tax directly. This mechanism aims to boost tax compliance and increase revenue, particularly in sectors prone to tax evasion and within the informal sector.

When Does RCM Apply?

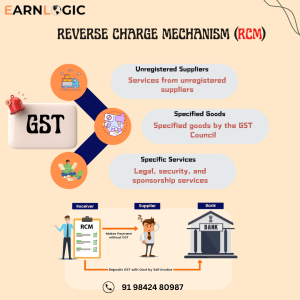

- Services from an Unregistered Supplier: If a registered GST holder receives services from an unregistered supplier, the tax liability falls on the recipient rather than the supplier.

- Goods Specified by the GST Council: The GST Council may specify certain goods subject to RCM, especially goods prone to tax evasion. In these cases, the recipient holds the responsibility for tax payment, even if the supplier is registered

- Specific Service Categories: RCM also applies to particular service categories, such as legal, security, and sponsorship services provided to corporate bodies, provided the service provider is unregistered.

Key Features of RCM

- Tax Payment Obligation: Under RCM, the recipient of goods or services must generate a self-invoice if the supplier is unregistered. The recipient directly pays the GST to the government and can later claim it as an input tax credit

- Compliance Requirements: Entities under RCM are obligated to maintain accurate records for all transactions subject to RCM. The recipient is responsible for compliance, including timely tax payments and maintaining proper documentation for purchases subject to RCM.

- Input Tax Credit (ITC): Recipients can claim an input tax credit for GST paid under RCM, provided the goods or services are for business use. This credit can then be used to offset future GST liabilities, thereby lessening the overall tax burden.

Impact of RCM on Businesses

- Cash Flow Implications: Under RCM, businesses must pay GST upfront and claim the input tax credit afterward, which can affect cash flow, particularly for small and medium-sized enterprises. Managing this aspect is crucial for maintaining liquidity.

- Increased Administrative Burden: The need to track which goods and services fall under RCM and ensure compliance adds an administrative layer to business operations. Accurate record-keeping and compliance checks become necessary to avoid penalties.

- Cost Considerations: The transfer of tax liability to the recipient may increase operational costs for businesses. Sectors heavily impacted by RCM might see a rise in compliance costs, which can affect their overall cost structure if not efficiently managed.

Examples of Services under RCM

- Legal Services: Legal services provided by advocates to business entities are generally subject to RCM if the service provider is unregistered.

- Transportation Services: Transportation services provided by non-corporate entities fall under RCM when the service provider is unregistered.

- Manpower and Security Services: Manpower supply and security services offered by unregistered suppliers to a registered person also fall under RCM, making the recipient liable for GST payment.

Conclusion

The Reverse Charge Mechanism is a significant component of the GST framework, helping to secure tax revenue at the point of consumption by shifting the tax responsibility to the recipient. While RCM minimizes opportunities for tax evasion, it also places the burden of compliance on businesses, which must stay vigilant about their tax obligations. Though the mechanism may influence cash flow and administrative efforts, businesses can usually reclaim the GST paid as an input tax credit. RCM, therefore, plays a crucial role in the GST landscape, promoting accountability and compliance across the supply chain.